Introduction

To support companies in developing climate reporting capabilities, on 25 August 2025, the Accounting and Corporate Regulatory Authority and Singapore Exchange Regulation announced that they have extended the timelines for implementing climate reporting (including external assurance) requirements as follows:

- Introducing tiered reporting timelines for issuers listed on the Singapore Exchange Securities Trading Limited (“listed issuers“) from the financial year (“FY“) 2025; and

- Implementing reporting timelines for large non-listed companies limited by shares with annual revenue of at least S$1 billion and total assets of at least S$500 million (“Large NLCos“) from FY2030 (instead of FY2027).

All listed issuers will continue to report Scope 1 and 2 greenhouse gas (“GHG“) emissions from FY commencing on or after 1 January 2025, while Straits Times Index (“STI“) constituents will continue to lead efforts to implement other International Sustainability Standards Board-based (“ISSB-based“) climate-related disclosures (“CRD“) from FY2025 and Scope 3 GHG emissions from FY2026. For more information on the original reporting requirements, please refer to our earlier Client Update on “Mandatory Climate Reporting for Listed Issuers from FY 2025, and Large Non-Listed Companies to Follow from FY 2027”, available here.

This Update provides a summary of these key revised requirements and timelines.

Revised Climate Reporting Requirements for Listed Issuers

With immediate effect, the revised climate reporting requirements are:

- A three-tier structure to phase reporting obligations based on market capitalisation:

- STI constituents;

- Non-STI constituent listed issuers with a market capitalisation of S$1 billion and above; and

- Non-STI constituent listed issuers with a market capitalisation of less than S$1 billion.

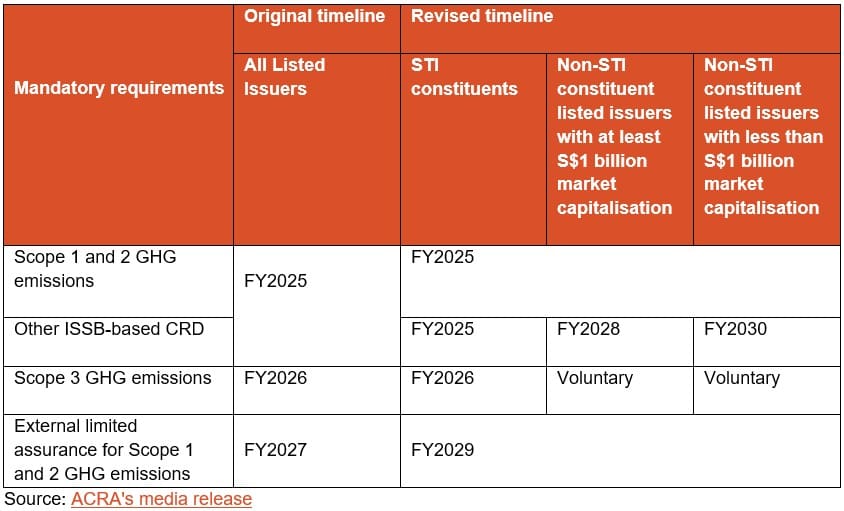

- Scope 1 and 2 GHG emissions reporting will remain mandatory for all listed issuers from FY2025.

- Scope 3 GHG emissions reporting will remain mandatory for STI constituent listed issuers from FY2026. For other non-STI constituent listed issuers, Scope 3 GHG emissions reporting will be voluntary until further notice.

- Other ISSB-based CRD (beyond Scope 1, 2 and 3 GHG emissions) will remain mandatory for STI constituent listed issuers from FY2025. Non-STI constituent listed issuers with a market capitalisation of S$1 billion and above will be required to report other ISSB-based CRD from FY2028. Non-STI constituent listed issuers with a market capitalisation of less than S$1 billion will follow from FY2030.

- External limited assurance for Scope 1 and 2 GHG emissions is deferred to FY2029 for all listed issuers.

Summary of requirements for listed issuers

Revised Climate Reporting Requirements for Large NLCos

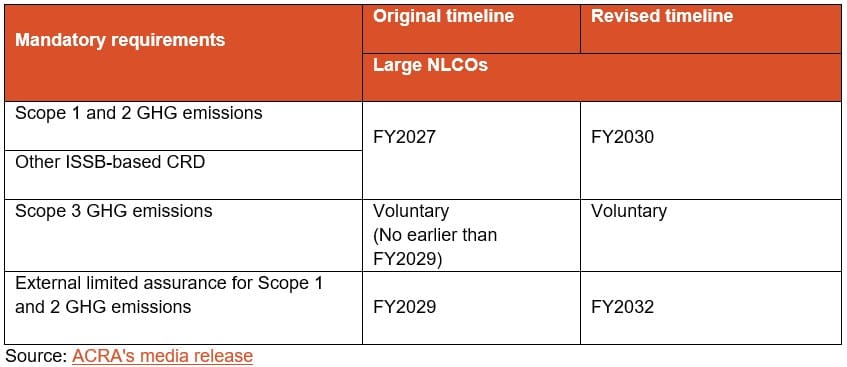

- ISSB-based CRD (including Scope 1 and 2 GHG emissions) are deferred to FY2030.

- Scope 3 GHG emissions reporting remains voluntary until further notice.

- External limited assurance for Scope 1 and 2 GHG emissions is deferred to FY2032.

Summary of requirements for NLCos

Our Comments

Companies are advised to prioritise readiness for Scope 1 and 2 disclosures, as well as use the extended timeline to build internal capabilities. Companies would also do well to establish governance frameworks now to avoid future compliance bottlenecks, as well as leverage available grants and training to prepare for future mandatory disclosures. In this regard, companies can tap on the Sustainability Reporting Grant by the Singapore Economic Development Board and Enterprise Singapore to prepare for Other ISSB-based CRD before mandatory compliance sets in.

Small and mid-sized enterprises keen to seek legal assistance related to sustainability reporting, climate and environmental governance can tap on our Environmental, Social, and Governance (ESG) legal fee subsidy under the Sustainability Legal Catalyst Programme with Enterprise Singapore (link to website). Terms and conditions apply. You can reach out to us at [email protected].

If you have any queries on the above, please reach out to our Contacts or KM at [email protected].